Seix Mountain View XIV Auction DNTs Amid Wider Spreads

The September 29, 2020 AMR auction for Seix Mountain View CLO XIV concluded without any of the subject tranches receiving a margin reset. Although multiple bids were submitted significantly below the margin cap, demand was insufficient to fill the full balance of any tranche.

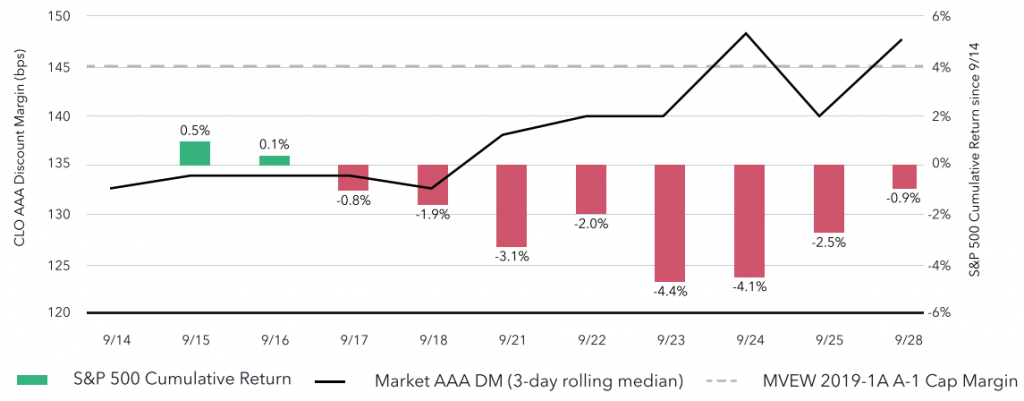

The culprit behind the diminished demand was the widening secondary market for CLOs; the Election Notice for this auction was sent on September 14. While CLO spreads continued to stay at post-Covid tights for about a week following the election date, equity market jitters finally caught up with CLOs last week. The S&P 500 Index fell as much as 4.4% during that time amidst rising uncertainty in the market. The secondary market CLO AAA spread (3-day rolling median) rose 14 bps from 133 bps to 147 bps during the 2 week period. The cap margin, which is the highest acceptable bid margin in an AMR auction, was set at 145 bps for the Mountain View XIV A-1 notes.

Secondary Market CLO AAA DMs Since 9/14

Source: KopenTech BWIC, KopenTech AMR, Yahoo Finance

Given that the median market AAA spread exceeded the cap margin in the days leading up to the auction, a successful AMR seemed unlikely. In this case, the majority equity holder decided to go forward with the auction to test the depth of the market and gain demand insights. Since AMR incurs no auction fees unless a margin reset occurs, there is no cost if the auction does not clear, similar to a DNT in secondary market BWICs.

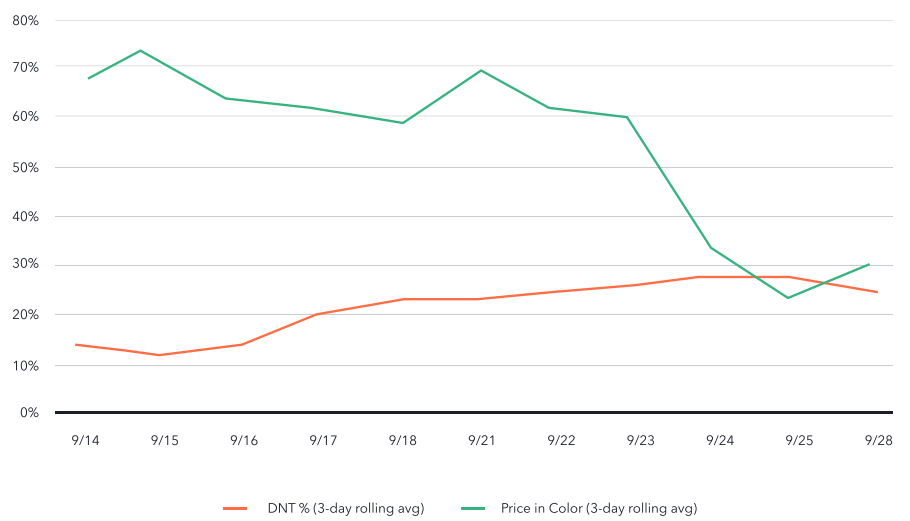

In the past 2 weeks, the secondary CLO market also began to suffer from liquidity problems. The BWIC DNT rate spiked from 13% on the AMR election date up to 27%. The proportion of trades where the seller offered price information (price-in-color rate) fell from 68% down to 24%. DNT rates are often used as a proxy for liquidity, with a high rate indicating an illiquid market. Price-in-color rates are used as a measure of market transparency, with high rates indicating an opaque market.

CLO BWIC Market Liquidity Since 9/14

Source: KopenTech BWIC

To monitor more CLO secondary stats, sign up at bwic.kopentech.com

Illiquidity and opacity go hand in hand. As securities become harder to trade in stressed markets, it is more difficult to find a consensus valuation (especially with structured products). Because valuation is more difficult, price information becomes immensely more valuable, and sellers often decline to share levels for this reason. This price opacity can then lead to even less liquidity as investor uncertainty grows. In fact, current secondary CLO market conditions are similar to the situation in March, when the onset of a pandemic saw a 26% DNT rate and a 17% price-in-color rate. Those figures are alarmingly close to the figures from this past week, further emphasizing the severity of the shock to the CLO market.

Although no tranches were able to have their margins reset, this auction highlighted one of the major benefits of the AMR feature: the collateral manager paid no fees for this auction, and it could hold another auction in as soon as eight business days if desired. In this regard, an unsuccessful auction is similar to a DNT’d BWIC: the seller pays nothing, price information is still gained, and the seller simply tries again without much effort. Had this refinancing been performed in the traditional manner, significant sunk costs would likely have been incurred.

KopenTech allows equity holders to test the waters rather easily because of its success-based fee structure. AMR has been accepted by market makers and investors alike. Fifteen broker-dealers are now signed up on the AMR platform, so investors have great access to a competitive pipeline to submit bids. With 8 other AMR CLOs active on the market, including 3 that are currently out of non-call, more AMR auctions may be right around the corner.